21st May 2020

Contributions to economics have been made by some of the greatest minds: Adam Smith (1723–1790), Milton Friedman (1912–2006), John Stewart Mill (1806–1873), Karl Marx (1818-1883), Joseph Schumpeter (1883-1950), John Maynard Keynes (1883-1946), Irving Fisher (1867–1947), Friedrich List (1789–1846), Thomas Malthus (1766–1834), Friedrich Hayek (1899–1992). The Nobel Prize has been awarded 51 times to 84 Laureates between 1969 and 2019. This collective knowledge forms and will continue to inform the foundation that constitutes the history of economic thought. It is unconscionable that this bastion of knowledge and collective intellect, to this day in the 21st Century, cannot comprehensively and consummately address the problem of poverty and inadequate resources. As Africans who bear the brunt of Western ideas in economics we must ask, despite this wealth of knowledge: why is it that poverty remains a challenge to humanity to this day? What is yet missing from this bastion of knowledge and collective intellect created by these great minds and highly credentialed and educated academics, as well as contributors who practice to this day, who are running key public and private institutions in areas such as currency, finance and development? What is at the heart of economics that over the decades and to this very day makes it permanently incapable of creating the wealth that lifts all of humanity out of poverty, strife and general economic malaise?

Missing from this history is the identification of flaws in the circular flow of income (CFI) that can be demonstrated empirically to cause financial losses referred to as subtraction or implosion identified in the Greater Poverty & Wealth of Nations (GPWN) that are equivalent to GDP per annum. Read how economics measures GDP over time (annually) and completely loses sight of losses in productivity that occur at any point in time – these losses are annually equivalent to GDP (read about this and understand it through an empirical test – here) .Because of the harm this over-sight causes humanity, it can legally be deemed professional mal-practice, once identified. Every student of finance, accounts, business and economics at any level, be it at secondary school, undergraduate, master’s degree, phd will graduate and enter a profession unaware of these losses in the CFI due to their identification being absent from the history of economic thought in which they are lectured and tutored. This in itself is a crisis of sorts. Without correcting and recovering these losses in the CFI they cannot in good conscience advise any government on how to create prosperity, without being disingenuous.

The GPWN shows that the underlying CFI has a flaw that creates an unaccounted for/invisible loss described as an Expenditure Fallacy (subtraction or implosion) equivalent to 100% of GDP per annum that occurs at any point in time. It diminishes useful economic resources for growth that leads to the phenomenon of cost plus pricing or the need for businesses to mark-up products by charging more for them than they are actually worth. The consequence of this loss is extremely low annual GDP growth rates observed in modern day economies.

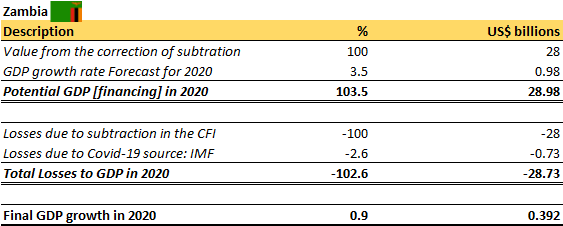

According to the IMF Zambia’s economy will experience a contraction in growth of “2.6% in 2020 from the earlier projection of 3.6%”

The table above shows financial losses caused by Covid-19 will be approximately 2.6% of GDP. Billions of kwacha have been earmarked to fight Covid-19, resources and man power have been mobilized and everyone is somehow involved in helping to prevent the epidemic.

This furor is for a problem with an economic loss to GDP of -2% to -2.6%.

Lets weigh this against the economic loss to GDP of subtraction in the CFI shown in the table which is -100% of GDP per annum. The value of this economic loss is almost 38x to 50x bigger than the economic loss caused by Covid-19.

Which begs the answer to the question:

Which is the bigger epidemic

People living in developing countries need to begin to provide answers to the problems related to poverty and underdevelopment the knowledge paradigm continues to fail to address.