3rd June 2020

1.1 This is a simple empirical test for law firms that will be admissible in a court of law before a Judge concerning systemic losses in income due to a defective economic operating system identified in the Circular Flow of Income (CFI) of a modern economy.

1.2 In addition, this empirical test is for CEOs, Directors, Managers, Lawmakers, office bearers and other leading implementors in organisations to ascertain, succinctly explain and provide justification for their decision to implement a Split Velocity system to a wider audience.

12.1 This test uses Zambian Kwacha, however, examiners are at liberty to replace this with the currency of their choice – K.

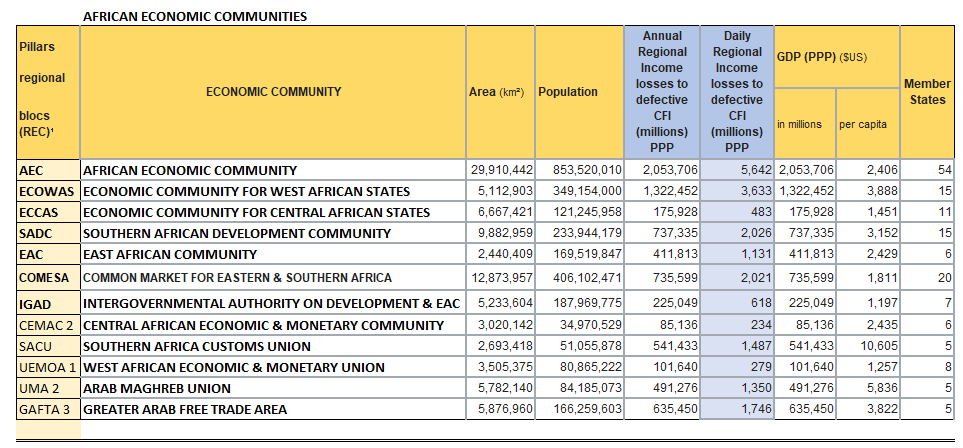

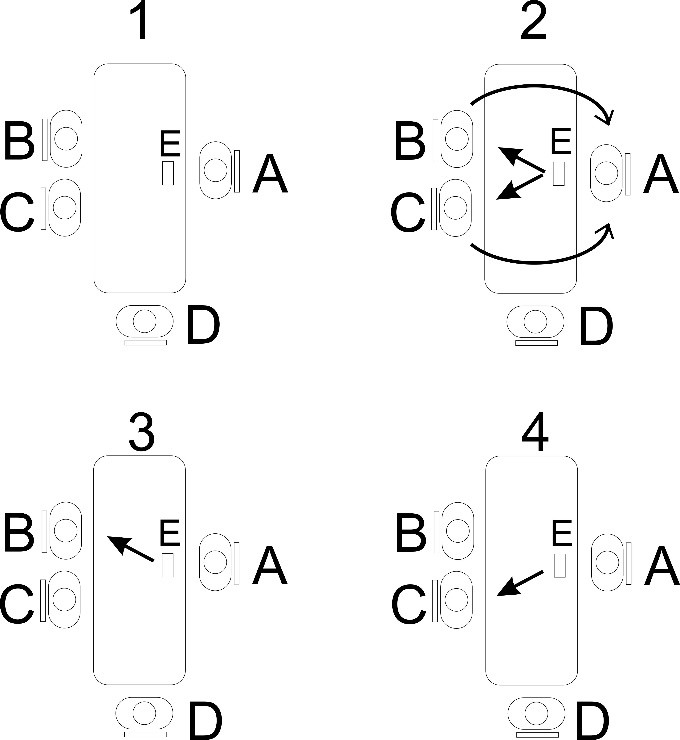

Empirical test diagram

1.3 KEY:

A – Test subject A: the Firm

B – Test subject B: Non-human capital (factor of production)

C – Test subject C: Households (human capital)

D – Test subject D: (Auditor*/Central Bank/Reserve Bank/Federal Reserve Bank)

*An auditor (e.g. KPMG, Grant Thornton, PWC, Deloitte&Touche, McKinsey & Company, Boston Consulting Group etc) or other competent firm/person can be used for this part of the exercise)

E – Stack of 10*K100 notes/Representative of Money Supply & Circular Flow of Income

K – Your currency e.g. Rands, British Pound, Yen, Yuan, Shillings, US dollar etc (use appropriate denominations)

Diagram 1: National economy with simple CFI

Diagram 2: Flow of money between the firm and households

Diagram 3: Allocation of income to non-human capital

Diagram 4: Allocation of income to human capital

1.4 Perform the Empirical Test using the test subjects:

- Set the test subjects as shown in the diagram. Test subjects A, B & C represent an economy or simple circular flow of income.

- The first test that should be performed is for the movement of money in the circular flow of income (CFI) or economic operating system (EOS) of the contemporary economy (CE).

- The auditor should make note in the ledger provided that test subject A holds 10*K100 notes amounting to K1,000.

- Have the auditor record the revenue held by test subject A

- Instruct test subject A to allocate 6*K100 notes to test subject B which amounts to K600. This represents 60% of the income originally held by test subject A.

- Have the auditor record the revenue received by test subject B

- Instruct test subject A to allocate 4*K100 notes to test subject C. This amounts to K400. This represents 40% of the income originally held by test subject C.

- Have the auditor record the revenue received by test subject C

- Have the auditor record the total value of money held by test subjects B & C

- Have test subjects B and C return the money they held back to test subject A

- Have the auditor record the revenue received by test subject A.

1.5 The test subjects represent a simple economy and the money moving between them a simple circular flow of income.

1.6 The value of output in this economy is K1,000. (The K1,000 income test subject A holds represents GDP).

1.7 Test subject A represents the firm. When he allocates K400 to test subject C this represents the firm’s payments to labour which consists of 40% of its total income.

1.8 When he allocates K600 to test subject B this represents 60% of the firm’s income allocated to capital. The duration it takes for the K1,000 distributed by the firm or economy to the factors of production (test subject B and C) and back to test subject A represent 1 year.

1.9 What this simple empirical test shows is that the value of income circulating in the economy between firms and factors of production remains constant at K1,000. This is a measurement of GDP over time [yearly periods] and what, to date, is currently understood in contemporary economics (CE) or Neo-classical Economics where the simple CFI is considered efficient and lossless.

1.10 We will now examine the same economy under the scrutiny of operating level economics (OLE) from the book the Greater Poverty and Wealth of Nations (GPWN) where the CFI is considered an economic “operating system” whose outcomes can be used to identify inefficiencies and financial losses they bring about in an economy. By correcting these inefficiencies these financial losses can be recovered and used to configure an economy to yield any results desired by which to improve economic performance. Recovering these financial losses from the inefficient and defective CFI provides new resources put to use in a more effective system for managing a national economy. This examination includes an analysis of the CFI using the standard analogue approach, which is over time, but delves deeper by including a digital analysis, that is, an analysis of the operations of the CFI at any point in time.

- Have the auditor record the revenue held by test subject A

- Instruct test subject A to allocate 6*K100 notes to test subject B which amounts to K600. This represents 60% of the income originally held by test subject A.

- Have the auditor record the revenue received by test subject B

- Instruct test subject A to allocate 4*K100 notes to test subject C. This amounts to K400. This represents 40% of the income originally held by test subject C.

- Have the auditor record the revenue received by test subject C

- Now have the auditor record the income that test subject A allocated to test subject C as income denied (a loss) to test subject B. This loss is referred to as Subtraction or Implosion.

- Now have the auditor record the income that test subject A allocated to test subject B as income denied (a loss) test subject C.

- Let the auditor add the total income lost by test subject C and test subject B in the final year column.

- Have test subject B&C return their money to test subject A.

- Let the auditor now add the year end income with the year end loss. Using this data let the auditor record the net economic gain after 1 year of economic activity. The result for this should be Zero.

1.11 What we have demonstrated with this simple empirical test of a simple CFI is that at the end of the year it experiences a loss in income or value equivalent to the money in circulation or GDP (100% of GDP) that is not accounted for in contemporary economics (CE). It is identified when the utilization of finance in the CFI is measured at any point in time rather than just over time.

1.12 Since we know that K1,000 is a measure of the value of output in the economy (GDP) this also represents a loss of goods and services worth K1,000 effectively dropping the productivity of money to a ratio of 1:0, that is for every K1 in circulation the yield or value of output is 0.

1.13 Businesses cannot survive in this condition created by the CE architecture, they therefore add price mark ups to their products in order to escape this architecture’s attempt to [shut them down] push them down to Zero profits.

1.14 In essence businesses naturally operate at a productivity ratio of 1:1, that is, for every K1 worth of GDP moving through the CFI they should expect a yield of K1 worth of output or growth, but instead, because of subtraction, despite their rate of productivity remaining constant at 1:1 what they experience is a yield of 1:0, nothing or no yield. This is why the present day neo-classical or contemporary economy (CE) is referred to as a Zero Growth economy.

1.15 Businesses therefore have to escape [the flawed CFI] the economy to survive. If their yield is 1:1.04 the economy will only grow by 4% because (1:1) 100% of their productivity will be eroded by the inefficiency of money caused by a dysfunctional CFI. This loss is currently not accounted for in neoclassical economics (CE) but is corrected in operating level economics (OLE) identified in the GPWN. It is the reason why modern day economies annually experience what can be described as mediocre GDP growth rates below 10% per annum.

1.16 Correcting Subtraction: The (SV-Tech) Split Velocity of Money

1.17 At this point you should now understand that in a system run on Split Velocity the productivity ratio for money is 1:1. This means that for every K1 moving through the operating system or CFI there will be a yield of K1 worth of output or GDP. For this segment of the test you will need two stacks each with 10*K100 notes. The first stack will represent money currently in circulation. The second stack of 10*K100 will represent raw money. (In total K2,000 will be required for this empirical test).

- Give the first stack of 10*K100 notes to test subject A

- Have the auditor record the revenue held by test subject A

- Instruct test subject A to allocate 6*K100 notes to test subject B (Non-human capital) which amounts to K600. This represents 60% of the income originally held by test subject A.

- Have the auditor record the revenue received by test subject B

- Instruct test subject A to allocate 4*K100 notes to test subject C (human capital). This amounts to K400. This represents 40% of the income originally held by test subject C.

- Have the auditor record the revenue received by test subject C

- Now have the auditor record the income that test subject A allocated to test subject C (Non-human capital) as a deficit in money supply and income denied (a loss) test subject B. This loss is referred to as Subtraction or Implosion.

- Now have the auditor record the income that test subject A allocated to test subject B (human capital) as income denied (a loss) as a result of a deficit in money supply for test subject C.

- Let the auditor add the total income lost by test subject A and test subject B in the final year column. This amount represents the systemic financial losses caused by operational inefficiencies in money supply created by the CFI of the contemporary economy caused by a money supply deficit.

- Now let the auditor take K400 from the income he was given to hold and give it to test subject B this represents a correction or restoration of money supply or income missing from the system. This is a correction [not an increase, since there is a pre-existing existing deficit] in money supply and it will take place at constant price.

- Let the auditor also take K600 and allocate this money to test subject C. Let him record the introduction of this money into the economy or simple CFI. [Split Velocity: The allocation of money to test subject B&C by the auditor who represents the central bank, reserve bank or federal reserve in this test corrects the money supply deficit, recovers the financial losses and repairs the inefficiency allowing money to move in two directions (Split Velocity), that is, to test subject B&C simultaneously restoring the systemic financial losses caused by the operational inefficiencies in money supply when allocations are made to the two factors of production by the firm.] It is important to note that this is a correction of money supply [not an increase in money supply, since there is a pre-existing deficit it does not represent an increase]. It will take place at constant price (growth without any inflation). The economic growth is pre-existent in the economy, it is simply not realized because the money supply to qualify it is missing from the economy as a consequence of subtraction. Technically, this means the correction of money supply in and of itself is not what causes growth, this growth is pre-existent in the national economy. However, it is lost when the inefficient CFI fails to balance money supply by countering subtraction and the yield or output as described earlier in the ratio of 1:1. This is why a Split Velocity model is counter-intuitive since when a perceived increase in money supply [correction of money supply] is observed, instead of a rise in inflation, the general price level remains constant and there is instead an increase in output or growth. In the empirical test B&C experience a deficit in money supply due to subtraction. The money supply is introduced to fill this deficit, it is not introduced as a surplus – with no real increase in money supply there can be no increase in price and therefore no increase in inflation.

- Now let the auditor take stock of the results after this correction of subtraction/implosion has been made. Let the auditor add the financial gains and make note of the total new year end financing which should consist of original GDP from year 1 plus the new financing made available by correcting the systemic deficit in money supply caused by subtraction. GDP after 1 year of augmented Split Velocity applied to the national economy to recover financial losses in the CFI should now be K2,000, that is, original GDP of K1,000 plus the additional GDP generated by correcting subtraction using augmented Split Velocity, that is, an additional K1,000 bringing the year end productivity or GDP to K2,000 at constant price.

1.18 This very simple empirical test can be extrapolated to any economy in the world to find systemic financial losses induced by operational inefficiencies in money supply caused by a dysfunctional or defective CFI. As can be identified by this empirical test, these losses are real and can be audited to provide evidence that can be used in a court of law. They are equivalent to GDP. Every economy in the world today experiences this real loss in revenue or useful financial resources that could have gone to education, health, the budget, paying off government debt, building massive infrastructure, ending underdevelopment, poverty and unemployment etc Instead countries lose this income, duly recorded by auditors in the simple empirical test, as pure waste to nothing more than a defective CFI. This flaw in the CFI costs governments billions of dollars worth of useful income every day, year in year out. As brought into evidence in the first part of the empirical test, this loss is hidden, unseen and currently unaccounted for in neoclassical economic theory (CE). These losses in income caused by subtraction in the dysfunctional CFI are therefore generic, unaccounted for and experienced by every economy in the world today. These losses are directly responsible for loss of life due to insufficient access to services, and critical resources such as medical supplies, chronic poverty, unemployment and general strife experienced by citizens on a daily and annual basis.

…………..

It should be noted that these inefficiencies identified at both macro and micro levels create an ongoing deficit in money supply that causes disequilibrium within firms between capital and households. This is money currently missing from the accounting processes and balance sheet of firms the absence of which is identified by the audit process. The restoration of this income to the balance sheet is strictly not regarded as surplus income, subsidy, endowment or grant to firms because it is the removal of a structural deficit by way of the correction of the CFI leading to the restoration of missing income owed to firms, required by firms for the normalization of productivity and the effectiveness of their day to day operations. The absence of this income can be characterized as ongoing “financial malnutrition” leading to a mediocre or low economic growth rate that is causing stunting which is hampering or crippling the effectiveness of their operations. On the macroeconomic level and where monetary policy is concerned it is not an increase in money supply since audit reveals this money is missing from the CFI, and it is therefore a mandatory correction of money supply and a correction of relevant economic indicators which includes the normalization of GDP, growth and output levels in an economy.

1.19 Credit creation does not prevent subtraction. If injections and withdrawals from credit creation, taxation and government expenditure were added to move this CFI from simple to complex these finances would still circulate through businesses and subtraction would continue to take place making it redundant to add these to the simple CFI.

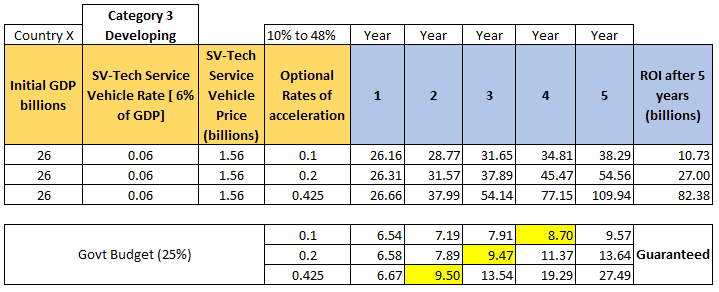

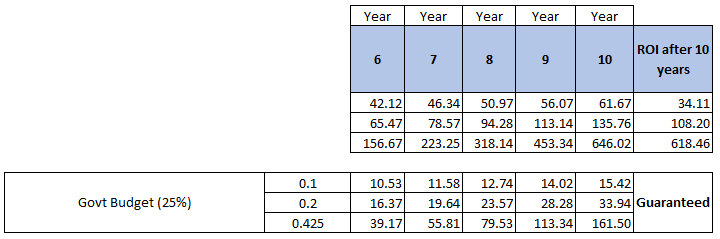

1.20 This method has been deliberately used to test through experimentation or a repeatable test how an inefficient CFI or operating system causes unseen financial losses to any modern-day economy. This simple method is ideal for this empirical test as it is easy to understand and can be digested by both professionals and laypersons of economics, accounts, finance and business. To apply this test to Country X swop K1,000 with Country X’s (your country’s whether developed, middle income or developing) current GDP.

1.21 Using the same basic principle that the simple K1,000 GDP replica economy we created for test purposes and its CFI was able to be financed by correcting subtraction, we will use the Split Velocity system to raise financing equivalent to GDP for country X (i.e. K249.6bn or $25.8bn) per annum, at constant price for the Country X economy. The funds the Split Velocity systems recovers from the inefficient CFI for country X exceeds all of country X’s current liabilities including both its domestic and international debt (US$14.7 billion) which could be paid off easily by upgrading the country X’s economy to a Split Velocity system. A debt liability of US$14.7 billion (60%) of GDP is nothing in comparison to the capacity of country X to recover as much as US$25.8 billion or the equivalent of GDP per annum from losses to the defective CFI for which evidence in provided in the empirical test.

1.22 A simple and effective empirical test that can be replicated in any setting

1.23 As much as we realise that much more sophisticated methods of testing, mathematics, statistics, equations and models are available and can be used to qualify what we have demonstrated here, it is felt this complexity would not be helpful as it would merely make a system that can be easily explained using basic fundamentals difficult to both convey and understand to laypersons. A simplified explanation divulged in an experiment, as has been provided here, that can be repeated for empirical analysis is expedient to express the required empirical evidence in a manner that is succinct and that can be understood by a wider audience which gasps simple functions of allocation, expenditure and loss .

1.24 We estimate that the daily losses to Country X’s economy caused by subtraction in 2018 at US$68.8m (K825.6m) per day. This represents a loss in finances that should be put to work in the economy. It represents loss of income for businesses. This is income that is taxable when recovered and it therefore represents a significant loss of revenue for government. These resources can be recovered to mitigate against the challenges currently faced by the Country X. It is therefore recommended that this condition receive immediate action by the Central Bank and National Treasuries/Ministries of Finance.

- There is a Legal basis and moral imperative for Split Velocity

2.1 A Legally admissible evidence based empirical test

2.2 This empirical test of a simple CFI can be introduced in court before a judge anywhere in the world as evidence of systemic financial losses caused by operational inefficiencies in money supply. Having been made aware of these losses, it is the legal, moral duty and fiduciary responsibility of office bearers to act to prevent, mitigate against and recover these losses.

2.3 No court, congress or parliament of law givers, anywhere in the world, would allow financial resources, on the scale being lost by the modern-day CFI to continue.

2.4 A simple CFI is representative of exactly the way the national economy operates. The losses observed in the empirical test are the very same losses being incurred by the national economy. Since these losses are systemic and caused by operational flaws they can be easily rationalized, analysed and empirically assessed by a simple model.

2.5 When a government makes a switch from the current neoclassical economic system to a Split Velocity system the changes and improvements in the economy will be profound.

2.6 No economy in the world today knows what its like to live and be active in an economy in which scarcity (as a systemic problem caused by inefficiencies in the CFI) has been removed or neutralized.

2.7 An end to poverty and strife caused by scarcity is anticipated.

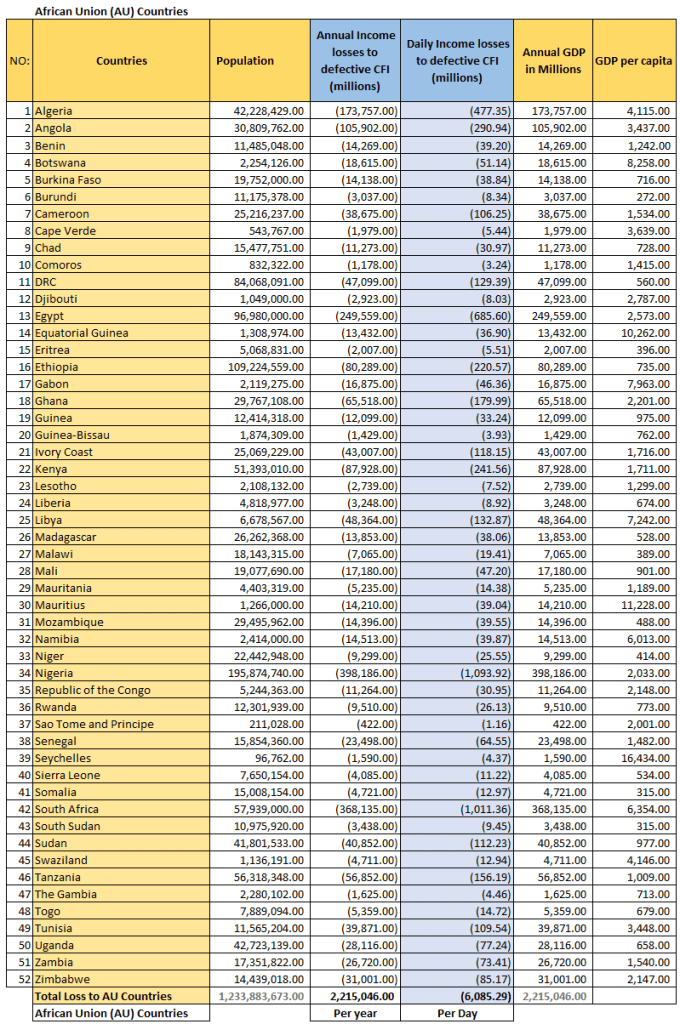

2.8 A dramatic improvement in the quality of life of citizens is expected when this transformation occurs. The tables below show the current losses being incurred by African nations due to a dysfunctional or defective CFI. As demonstrated by the empirical test, the losses in the tables are not hypothetical losses, they are real financial losses that can be audited.

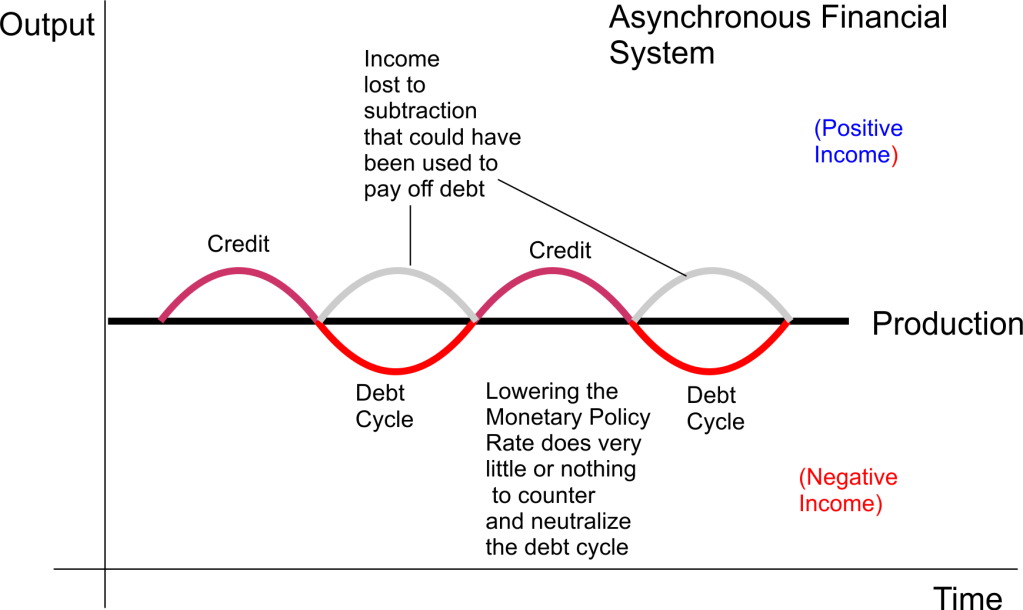

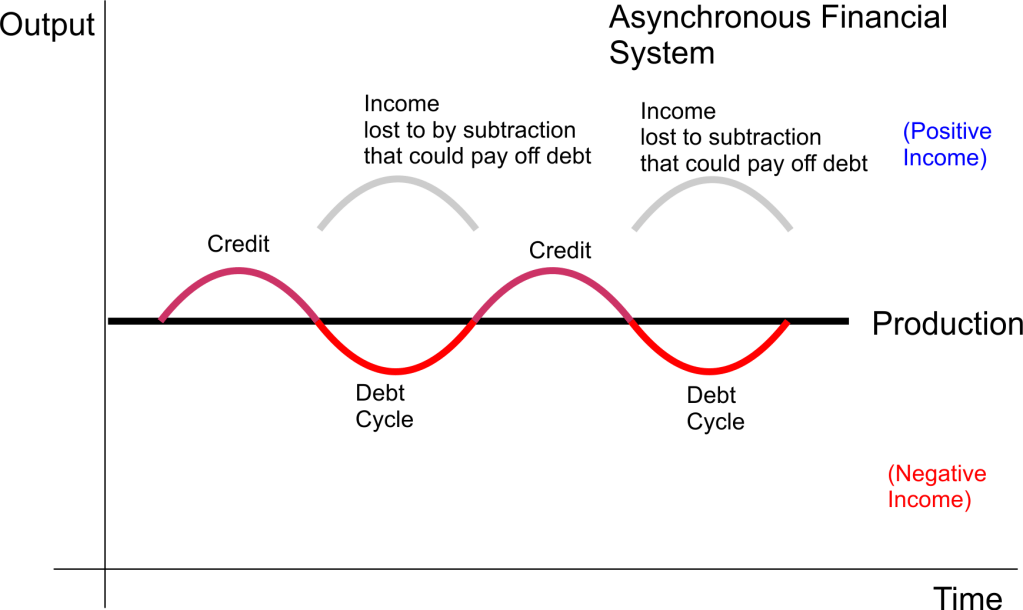

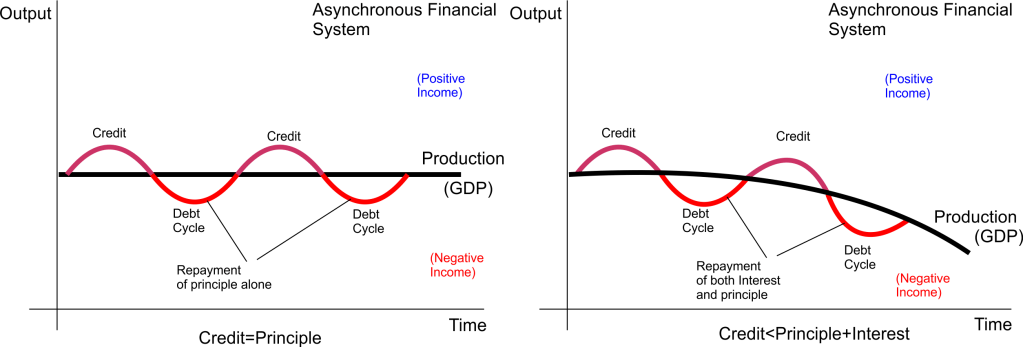

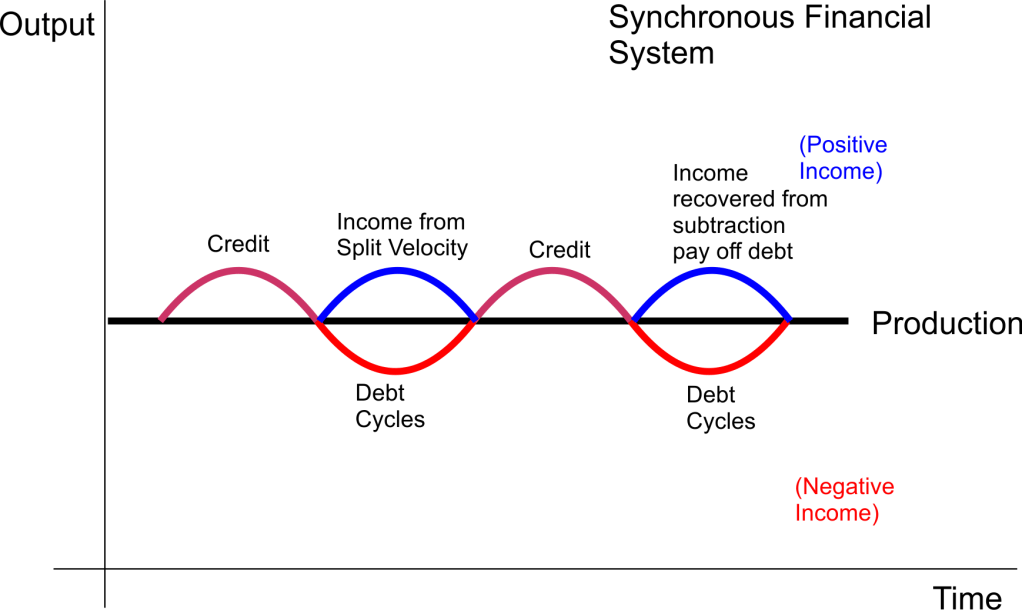

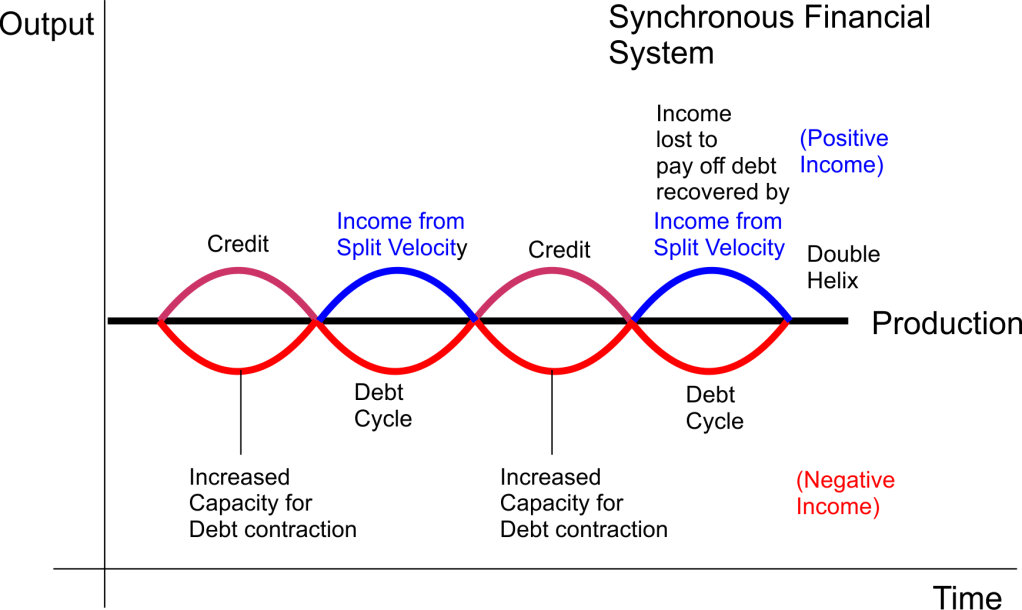

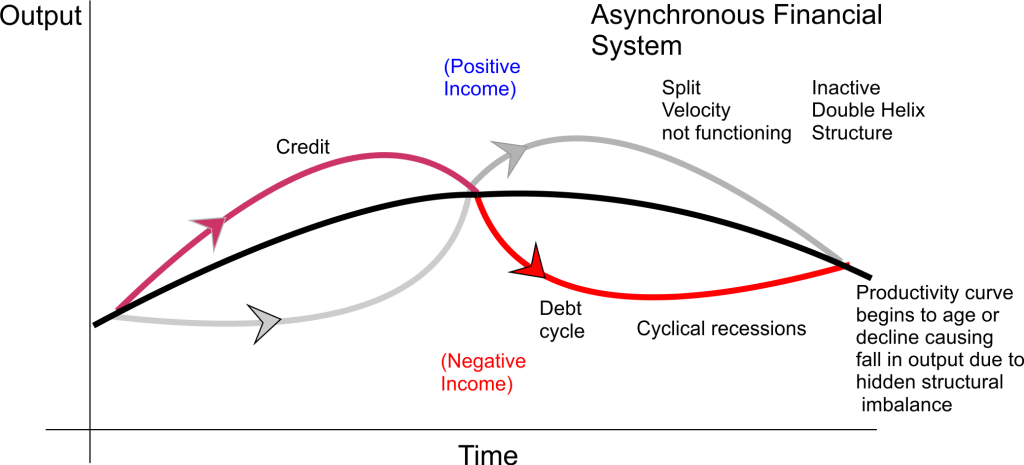

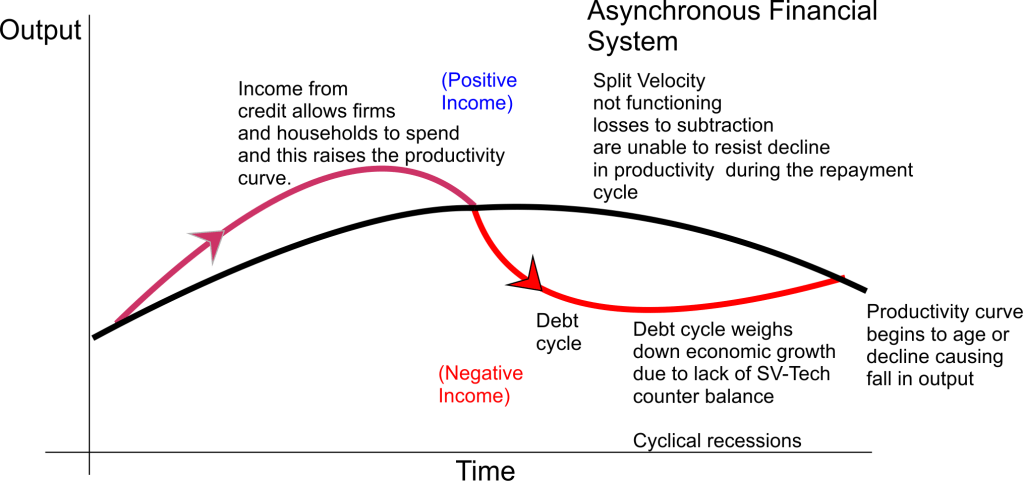

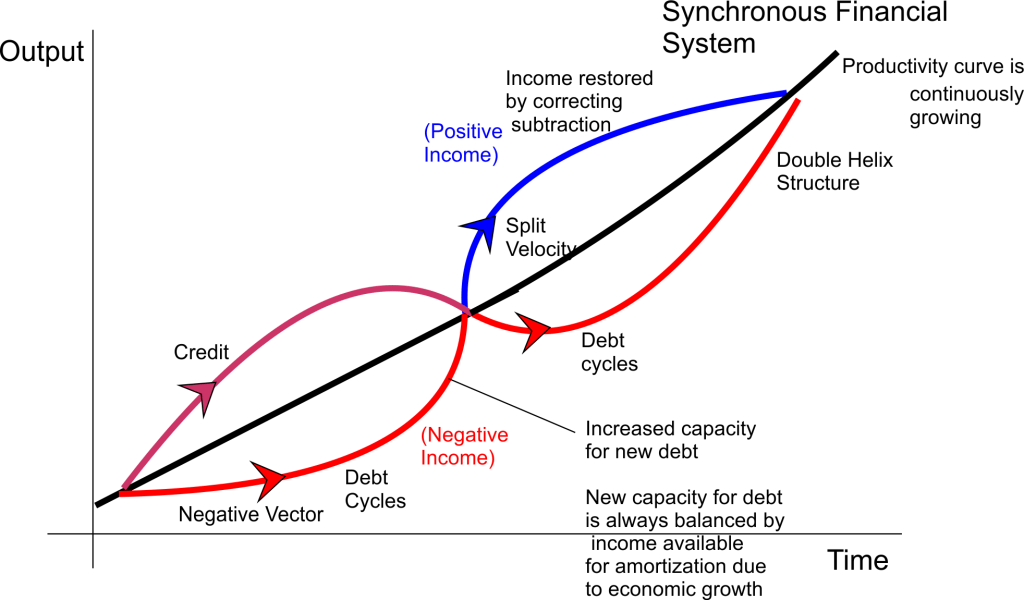

2.9 An Asynchronous financial system makes it exceptionally difficult to manage and repay debt for both individual borrowers as well as governments. A dysfunctional CFI offers a technical explanation for why despite debt cancellation through initiatives such as HIPC and access to domestic and international credit with which to create growth the flawed CFI places countries at a high risk for finding themselves back in distress when they try their very best to steer and manage a national economy toward prosperity for the people. It is also important to understand that the financial resources recovered from subtraction move an economy from having an Asynchronous system in which demand for credit is low and the default rate is high to having a Synchronous financial system where the demand for credit is much greater but is balanced by the growth in the economy required to amortize loans, thereby causing a reduction in the default rate and lower risk in the banking sector (to see Understanding why Split Velocity complements Credit Creation 26th May 2020, below click here). An SV-Tech system involves counter intuitive processes, and for some (even though they may have graduated very recently from university and other higher institutions of learning – at the highest or any level of qualification), retraining may be required for the outcomes to be clearly grasped.

………