26th May 2020

When governments, businesses and people borrow from local banks and international creditors their spending power or income improves. However, since these are loans there comes a time when the debt must be paid back. To pay back debt debtors must dig into their income to settle what they owe, which means they may have little disposable income left.

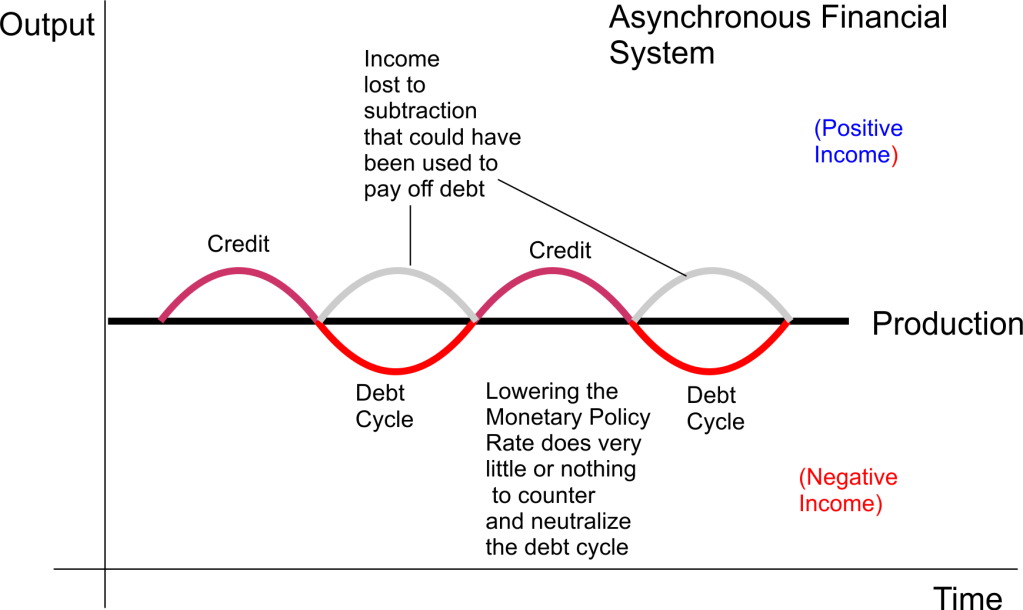

There can be ongoing analysis and debates on debt accumulation and amortization. Unfortunately very little attention is paid to systemic weaknesses pre-existent in the financial system that negatively skew the capacity of governments, firms and households to manage debt. One of these weaknesses is the debt cycle, its tendency to compromise amortization and its capacity to trigger unnecessary recessions when growth in a national economy encounters a bump in the road. Continuous borrowing over time and repayment creates a debt cycle, as shown in the diagram below:

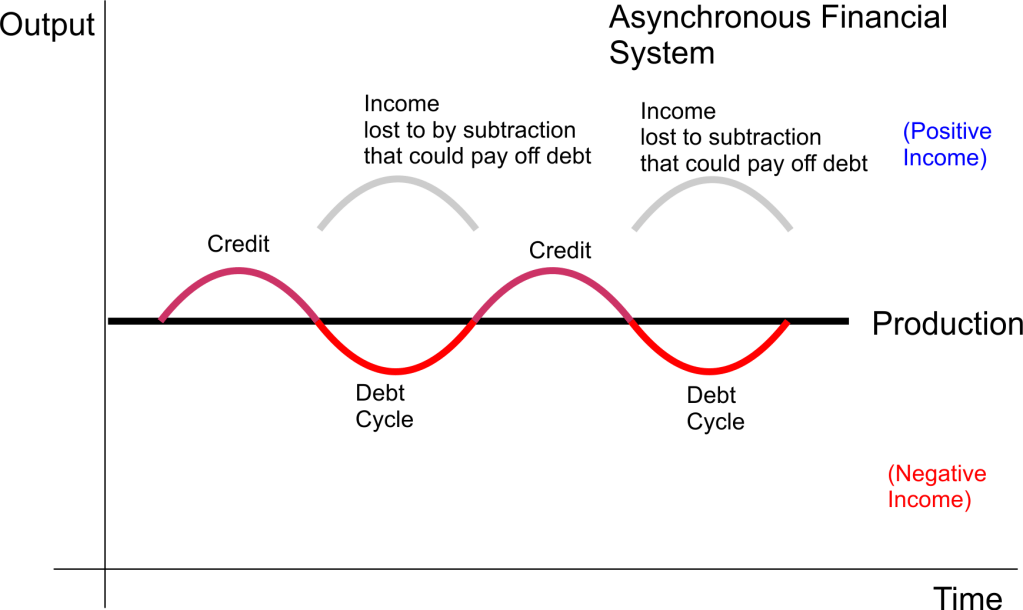

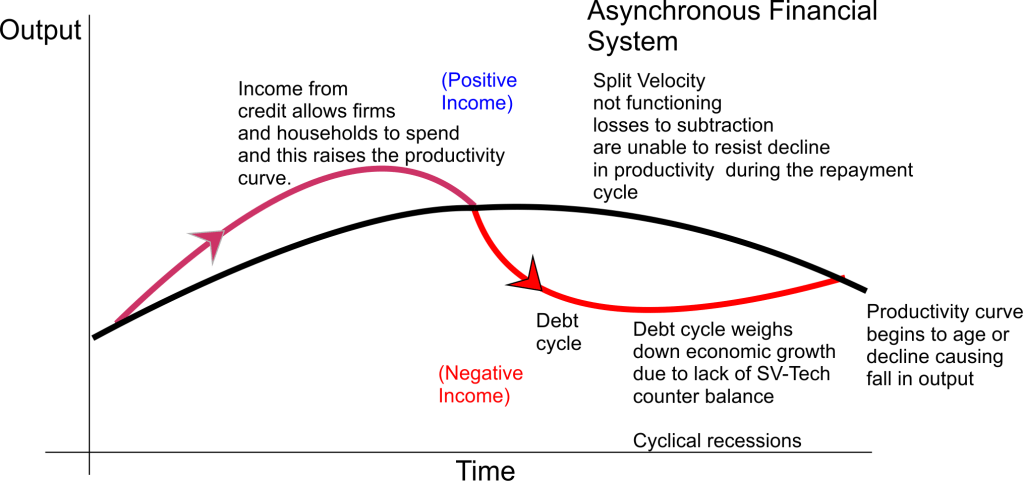

The relationship between credit and debt is Asynchronous since when credit is taken, debt is paid back at a later date. When borrowers pay back debts they experience a loss of disposable income. Its as though this income, which goes to settling debt does not exist to the household’s microeconomy and to governments domestic obligations. When we lift income lost to subtraction as shown by the gray arcs in the graph the Asynchronous relationship (shown in the red curve) becomes more visible. If we approach this the way we view epigenetics in the study of the structure of DNA (like DNA the underlying systemic or operating structure of an economy can make some of its outcomes predictable such as high default rates and recurring recessions), in essence it means that despite being visible sections of DNA are inactive. This inactivity or lack of activation, like subtraction in the circular flow of income (CFI) at the operational level, creates an imbalanced or Asynchronously functioning double helix or economy. As shown below with nothing to counter-balance the red curve (or single section of a helix) the economy becomes prone to debt related problems, such as those being experienced by a country like Zambia in 2020:

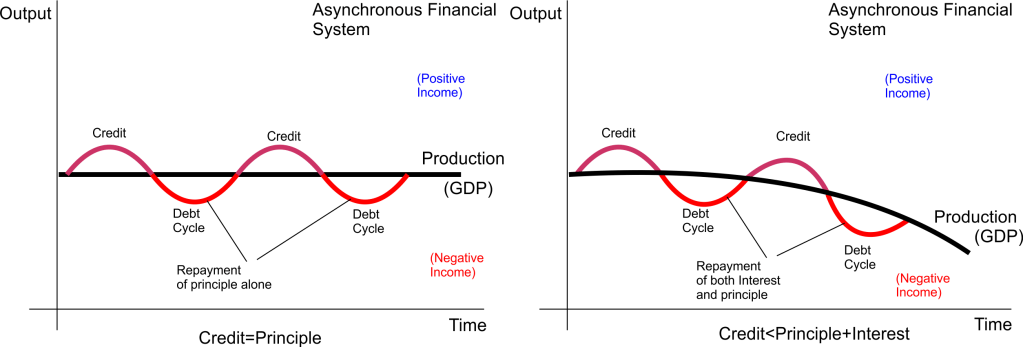

The Asychronous debt cycle curve above shows that if the amount of credit issued in the economy is equal to the principal owed and paid back at a later date then technically credit creation is injecting the equivalent value of money it receives. Therefore, the productivity curve is a straight line. Technically this means that credit creation is not directly responsible for economic growth. However, it is a common fact that debtors don’t just pay back the principle, they also pay interest on loans. This entails that credit creation during the debt cycle withdraws more money from productivity than it gives out. If this is the case, the weight of debt on the productivity curve or GDP is heavier thereby weighing down on rather than aiding economic growth.

In an Asynchronous financial system for the economy to grow firms must

overcome the weight of the debt cycle in order for GDP to rise. If the

Return on Investment (ROI) is lower than the debt burden the economy

will experience negative growth. Technically, this illustrates

that though credit creation gives firms money for investment

it does not create economic growth, businesses have to work for this growth

against the weight of debt, uncertainty and risk prevailing in an economy. This explains

why Split Velocity is a critical piece of the puzzle required by the banking industry

expedient to how governments manage the national economy.

Split Velocity (or wealth creation as a financial product when experienced by the end user) works hand in hand with credit creation to create a much better performing environment for loans because it pushes growth, minimizes credit risk and reduces uncertainty in the financial sector, which is what credit creation needs to function properly allowing it to consistently create positive rather than negative growth.

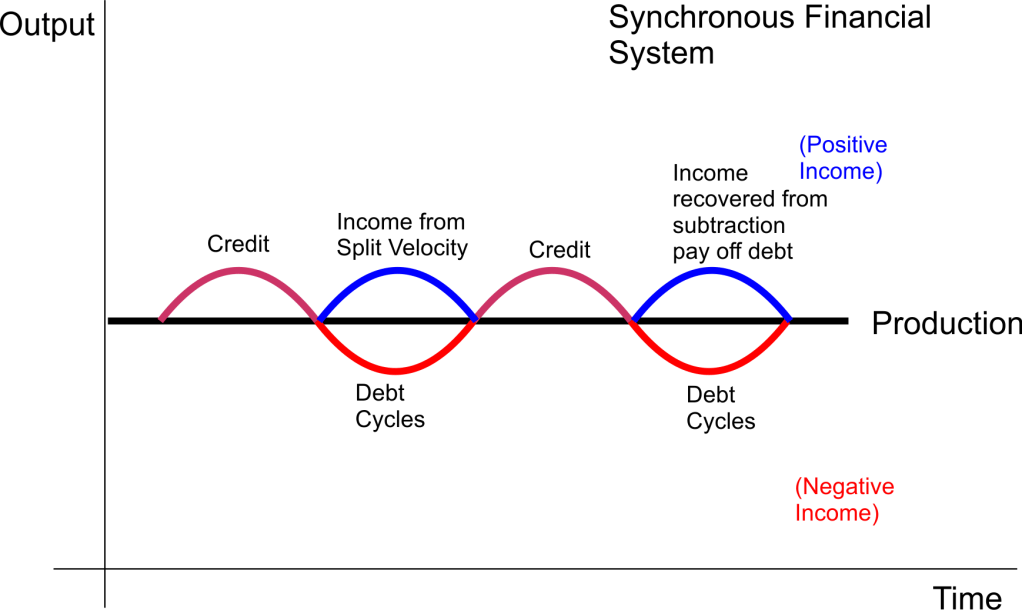

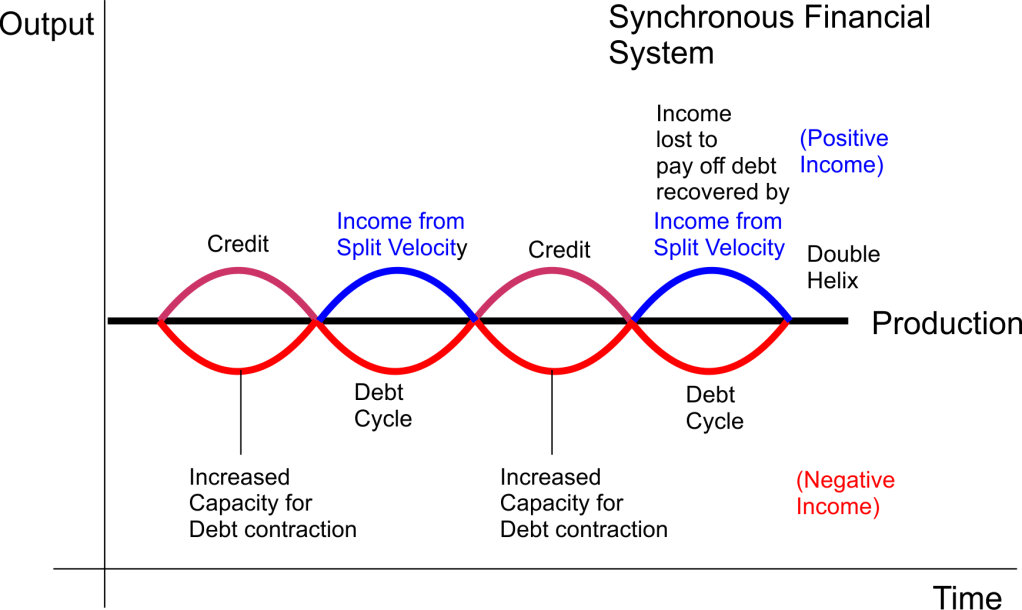

When we introduce SV-Tech (Split Velocity) to an economy what it does is it restores the income being lost to subtraction. This means that income that government, businesses and people are losing that could be used to repay debt can be replenished or restored. During the periods in the cycle when government, businesses and households have no income to pay off debt this vacuum can be covered by income recovered by Split Velocity. This changes the economy from being Asynchronous and prone to debt cycles to being Synchronous and resistant to the negative impact of the debt cycle, thereby bringing an end to recessions triggered by debt. This neutralizes the default rate (rate at which loans become non-performing as a result of debtors being unable to repay their debts.)

debt with the income gained to repay it consequently

protecting commercial banks from defaulting clients.

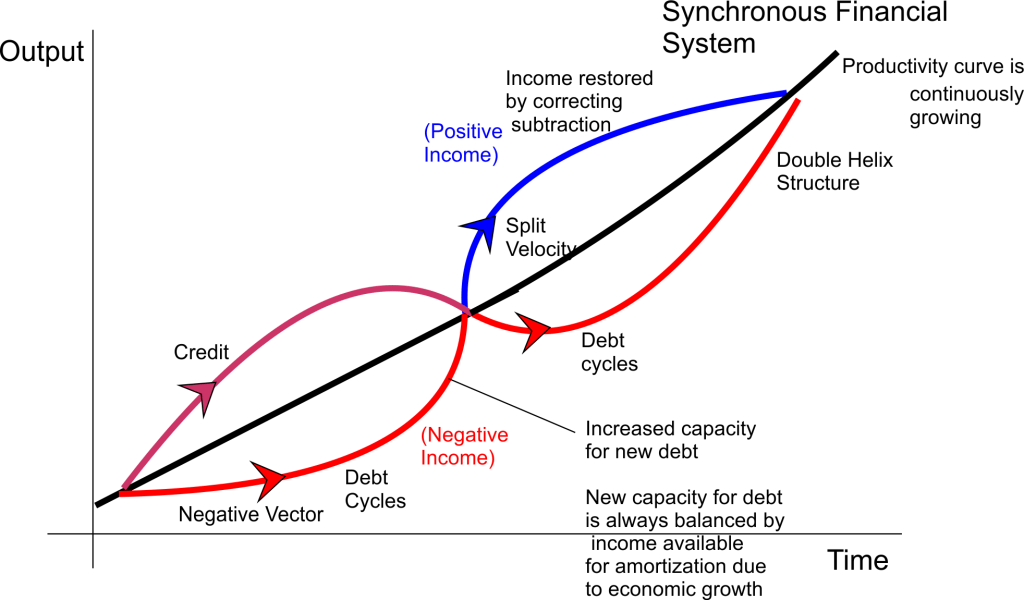

The income gained from correcting subtraction increases the credit worthiness of borrowers. The consequence is that they can now take on more debt. An SV-Tech system naturally leads to an increased demand for loans due to the fact that creditworthiness (rather than desperation or desperate circumstances) is what increases the demand for loans; government, businesses and people feel comfortable about taking on more debt due to the fact that they feel more capable of paying it back. The activation or increase in debt contraction is shown in the diagram below:

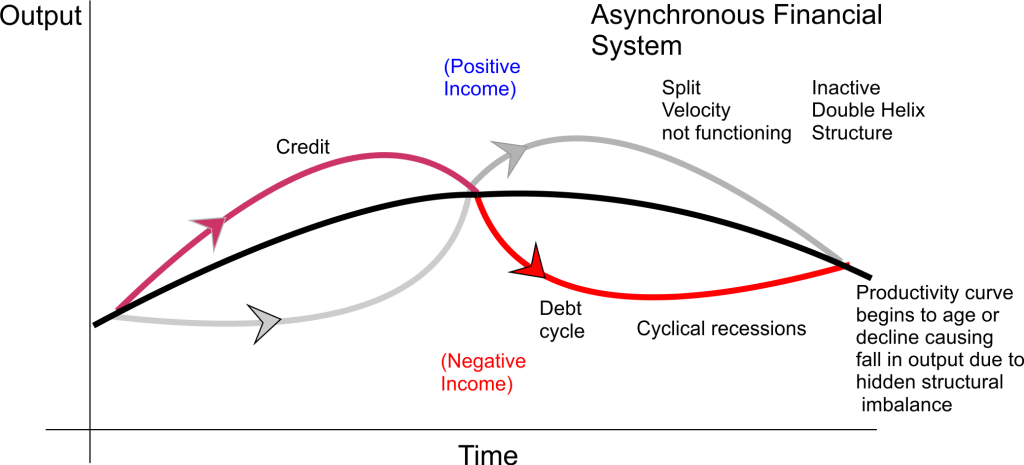

The effect of disharmony between strands (the operational level of the economy), the upper and lower structure or tension between income available for amortization and debt has a negative impact on output or the productivity curve as shown in the diagram below. When government, households and firms are unable to pay back debt because they do not have the [Synchronous] income the default rate rises pushing the economy and banking sector into deeper crisis. The negative consequence is a downward sloping production curve as goods and services remain on shelves due to a drop income caused by debt servicing or productivity slows due to debt not being amortized. This creates a catch 22 in that whether a debtor like government pays its debt or not there are negative repercussions. This pushes debtors to try to borrow yet again, now out of desperation, through government instruments, commercial banks or multilateral institutions such as the IMF. In essence, the sad reality is that the systemic problem that exasperates amortization of debt that helped create these hurdles in the first place is not being addressed. An Asynchronous financial system is poorly designed, inefficient, generally unhealthy and inadvertently makes it difficult for economies to manage debt.

The Asynchronous nature of the economy and its impact on the production curve (GDP) is shown more clearly below. The negative impact of debt drags down productivity and output begins to decline because it is not being balanced with the productivity levels that finance amortization.

The diagram above shows that the central bank lowering the monetary policy rate is not always an appropriate stimulus for an economy facing a downturn as it tends to add more weight to the Asynchronous downside of the economy at a time when both firms and households are reluctant to borrow because they are afraid the deteriorating economy may hamper their ability to amortize loans. (This is like pouring more water [debt and inflation] into a half empty lake (recession) where people are drowning, in the hope that more water will make them better swimmers.) However, when Split Velocity is introduced to an economy it harmonizes the [Asynchronous] imbalance between credit and debt (upper and lower structure of the economy). By making it Synchronous this ensures that there is no income vacuum during any period in the short term or long term when income is required for servicing loans. The result is, instead of a decline in confidence in the economy, confidence rises and growth instead begins to increase leading naturally to a rise in demand for loans from commercial banks as shown in the diagram below. Government also faces no difficulty in settling its debt obligations with local and international creditors and can do so without disrupting domestic economic activity.

This demonstrates that SV-Tech is a far more powerful tool for getting an economy out of a recession and triggers a greater demand for loans from commercial banks than the central bank lowering the Monetary Policy Rate alone even to its lowest level (filling the lake with more water), which is likely to have the negative side effect of causing higher levels of inflation while an economy is already struggling with a downturn. The success of rate cuts such as this are firmly dependent on how the economy will perform in the future. The SV-Tech system alows the central bank to achieve the same objective without uncertainty and without causing any rise in inflation.

economy to amortize debt is persistently backed by

economic growth. In other words whenever commercial banks

issue credit the growth required to ensure the economy has

the capacity to repay it grows with the debt burden. This creates

a much safer economic environment for creditors as it has a low propensity

for default .i.e. for non-performing loans.

The diagram above demonstrates that when commercial banks begin to operate in an economy managed using Split Velocity economic growth remains resilient and consistent to the extent that there is rarely a vacuum in income required to service loans. In an economy managed using an SV-Tech system growth is guaranteed and predictable using projections. Therefore, commercial banks, by knowing the growth rate in advance, can determine safe levels of credit to issue in the economy. These safe levels will be much higher than those available today. At present commercial banks issue loans with no real idea of how the economy will perform. They have to rely on prevailing economic conditions, indicators or unreliable forecasts and never really know how the loan portfolio will perform. SV-Tech mitigates against the risk of issuing loans. This is why SV-Tech (or wealth creation to the end user) compliments credit creation. Wealth creation and credit creation are complimentary products that ideally should function in the same space to ensure financial system stability. However, Split Velocity is for now missing from this space.

The reason why I chose to compare economics to genetics is to try to show you that how economies operate, like DNA, has specific outcomes. Poverty, scarcity, high levels of credit risk, unemployment are like symptoms of either damaged or inactive DNA. In a human being these cause aging, sickness, disease and so on. Fix the DNA and these symptoms come to an end. Similarly fix the operating system of an economy and modern day economic problems associated with scarcity end. The “operating system” of an economy is the “Circular Flow of Income” (CFI), this identity is made in the book “The Greater Poverty & Wealth of Nations”. The CFI is the operating system of an economy and therefore determines economic outcomes that determine the health of an economy, just like DNA. It implies that the shape of curves, and their symmetry or lack of it, determine outcomes.