11th May 2020

SV-Tech is able to shift debt contraction capacity from current GDP to projected GDP:

With SV-Tech governments can borrow with secure knowledge about how the national economy will perform. With growth rates set anywhere between 10% to 48% debts acquired have greater certainty of amortization.

Debt of this kind is “contracted”, meaning it is gained as a result of agreement [.i.e contract] between an entity seeking to acquire a loan (the debtor) and an entity that provides the service ( a creditor). The ability to take on more debt in this manner is therefore referred to here as “debt contraction capacity”, it can also be

referred to less technically as “debt carrying capacity”.

The enhanced debt contraction capacity shows that a Split Velocity model increases the demand for loans from local and international creditors due to the fact that borrowers will clearly see they are in a conducive economic environment to take on debt. [When banks receive money to distribute as loans in a downturn risk averse borrowers will tend to shun loans because they are afraid they can’t repay them. Even if they take loans the potential for default in a downturn is high. By using SV-Tech to improve the financial position of borrowers, they gain the confidence to take on more loans and actually repay them. An economy financed by SV-Tech will see increased demand for loans from commercial banks. This is a counter-intuitive process that works [see the advantages of an synchronous financial system here]

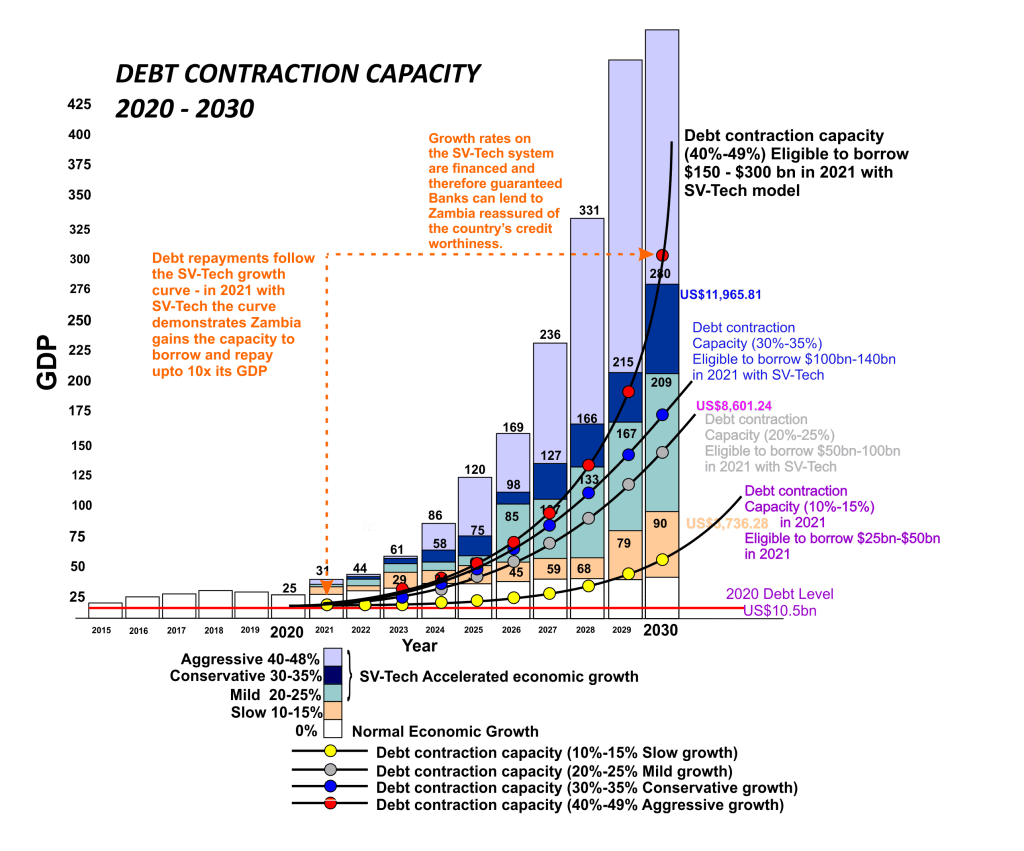

The diagram above shows that Zambia’s debt contraction problems are directly related to slow economic growth that is incapable of sustaining the economy’s needs. Recovering losses to subtraction which consequently accelerate growth leading to higher government revenue is the most practical method for addressing Zambia’s credit worthiness.

Since economic growth determines a county’s capacity to borrow from domestic and international markets, and SV-Tech has sovereignty or direct control of an economy’s level of productivity, this means developing countries have a pragmatic mechanism for guaranteeing the stability of the domestic currency. The diagram shows that by simply using SV-Tech to accelerate growth by 10%-15% Zambia’s debt position improves remaining consistently at 50% of GDP. This is however the slowest rate on the system. Accelerating growth to 20%-25% drops government debt to 25% of GDP through the decade. Should the central bank opt for an aggressive growth rate (which is what is recommended for poorer developing countries) the debt to GDP percentage becomes negligible or 10% and below. These improvements in debt contraction capacity open the doors to government renewed borrowing. If an aggressive setting were applied the Zambian government could look forward to issuing Euro-bonds for 2030 or later maturity valued at US$100 – US$150 billion and this would only be 10% – 23%of GDP. A Split Velocity model is much safer, recession resistant, more robust and significantly more secure than economies run without it.

Since the SV-Tech model predetermines the rate of economic growth the country’s credit worthiness can be based on the applied rate of acceleration with repayments following the growth curve. What this means is that despite Zambia’s GDP being US$28bn in 2020, should it have a Split Velocity model in place in 2021 its credit worthiness could rise depending on the growth rate applied, with the highest being an aggressive growth rate which implies the capacity to borrow and repay US$150bn – US$300bn in 2021, which is 10 times Zambia’s current GDP [see above curve where it shows “debt contraction capacity”] this ofcourse does not mean the country should borrow 10x its GDP, rather it demonstrates that credit-worthiness can be leveraged by the SV-Tech system allowing a more robust demand for loans that are now easier to repay, which in turn leads to a significant back-stop for balance of payments. This in turn will restore the value of the Kwacha and act as a buttress for the general price level that is now stable over the long term. The consequence of this is highly and effectively enhanced financial system stability. The ability to achieve these results are what exemplify best practice in central banking and they are achievable by central banks facilitating the introduction of an SV-Tech system to an economy”.

This demonstrates that the real problem is not debt per say but the creation of growth and economic conditions that are conducive for borrowing and repaying government debt such as that created by a Split Velocity system.

Few other (if any) approaches to economic management would yield results credit rating agencies such as Standard and Poor, Fitch Group and Moodys might find conducive for growth, stability and a robust international credit system.